Institutional Crypto Trading Platform

Our Institutional Crypto Trading Platform Solution

Wyden ensures best execution through market-wide connectivity and end-to-end crypto asset orchestration. Seamless integration with premier custody, core banking and portfolio management system providers make Wyden the leading institutional crypto trading platform covering the entire trade lifecycle for digital assets.

Best execution during the entire crypto asset banking lifecycle.

- End-to-end trade automation across the entire lifecycle of principal and agency trading

- Risk- and commission-optimized order funding and settlement with seamless integration of core banking systems and custody solutions

- Designed to flexibly scale with your crypto banking strategy

Our Modular Institutional Crypto Trading Platform Offers Custom Solutions

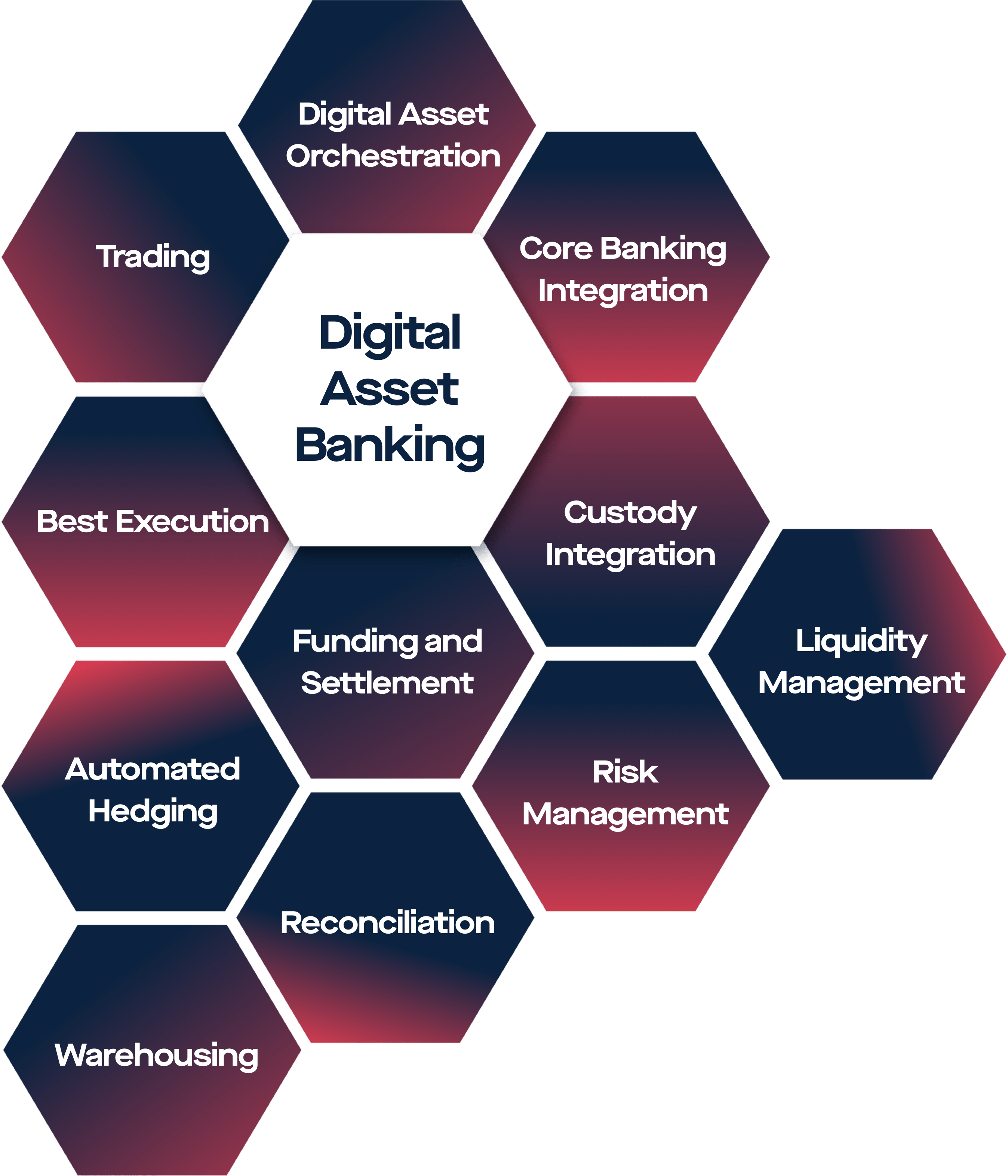

Crypto Banking

Wyden’s institutional crypto trading platform seamlessly integrates with custody solutions and core banking systems to offer diversified connectivity and best execution for banks. Using Wyden, you can offer crypto banking services through your own brokerage desk, which automates the crypto trade lifecycle end-to-end, minimizes counterparty, operational and market timing risks, while leaving you in full control of every step of the value chain.

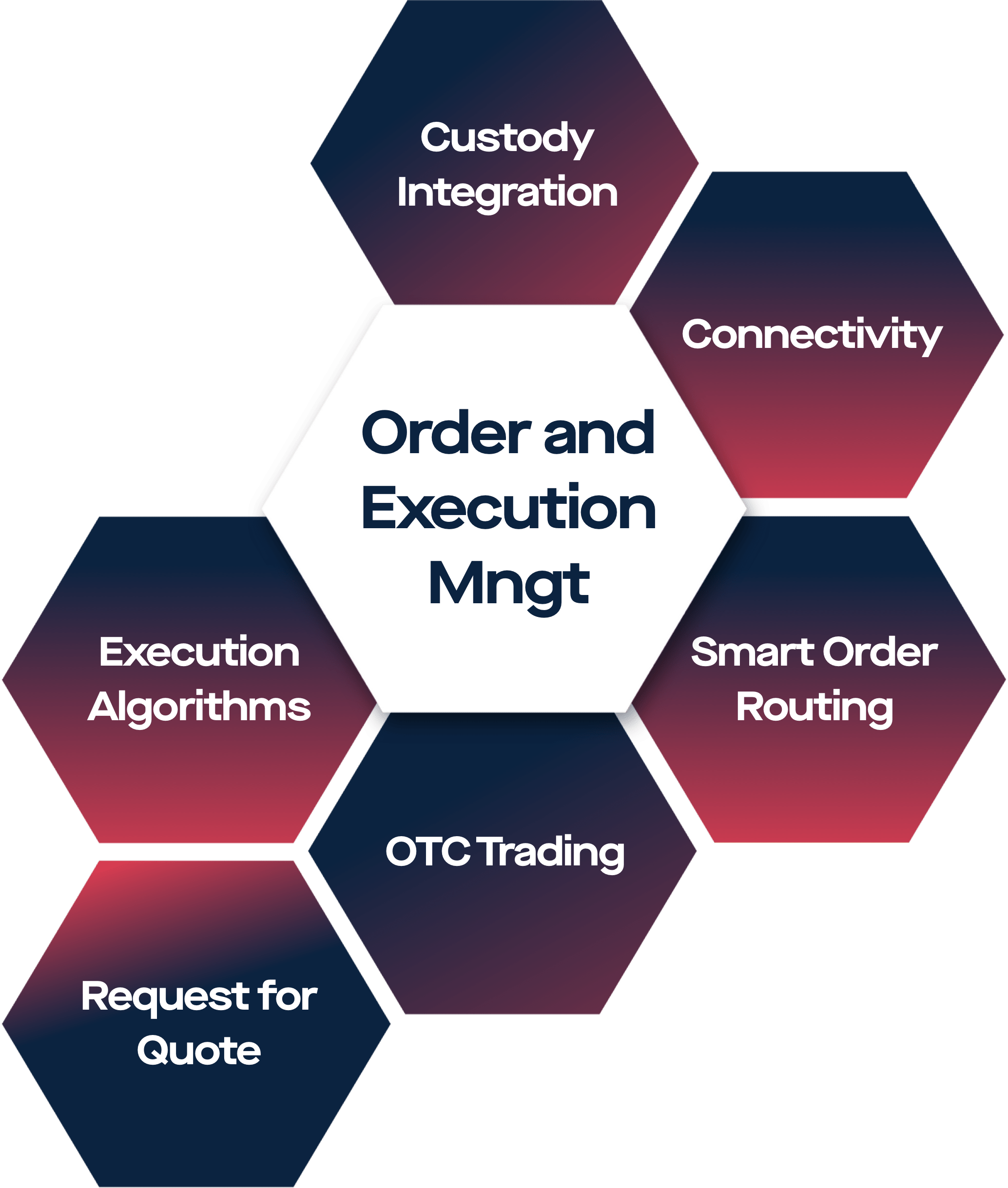

Order and Execution Management

Discretionary and systematic buy-side institutions benefit from our fully integrated portfolio, order and execution, and position management system for crypto assets. Wyden’s advanced smart order routing (SOR) and execution algorithms enable you to efficiently scale and streamline your trading operations by automating every step of the process — from pre-trade funding, to execution, and post-trade settlement.

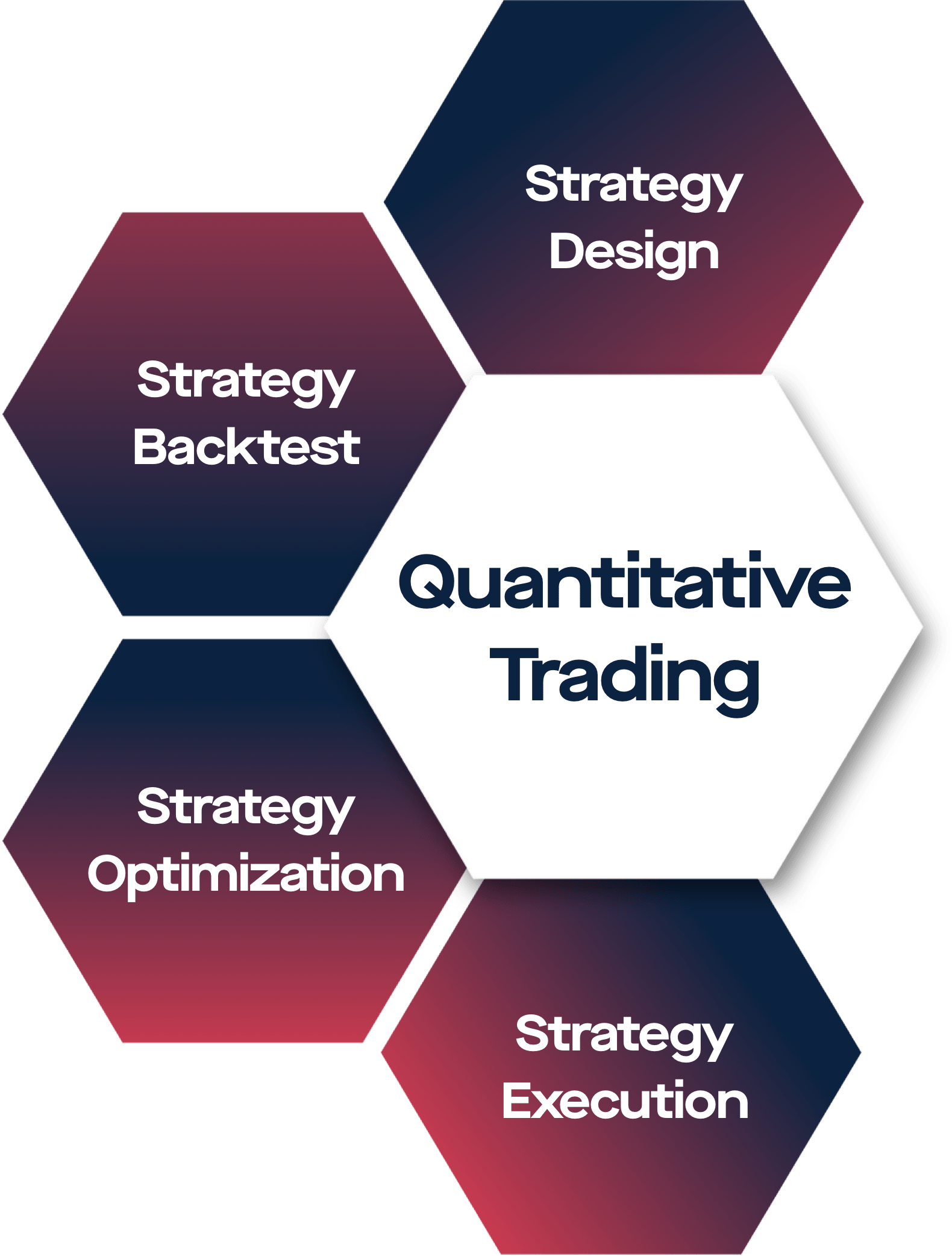

Algorithmic Trading

Wyden provides an end-to-end algorithmic trading platform, covering everything from generating algorithmic trade signals, to automatically executing orders. Use the integrated development environment to build any type of custom algo strategy – or let Wyden’s team of experienced strategy developers do the job for you.

Our Institutional Crypto Trading Platform Offers Single Access to Global Liquidity

Market-Wide Access to Crypto Assets

Connect to the largest centralised (CEX) and decentralised (DEX) crypto trading venues, traditional asset exchanges and market data providers.

Managed Connectivity

We eliminate any REST & Websocket related issues of crypto trading venues.

Best Execution

Smart Order Routing and advanced execution algos ensure trades get filled at the best conditions across multiple venues.

35+ major crypto exchanges,

brokers & OTC desks

Spot | Options | Futures | Perpetual Swaps

Explore Venues15+ largest traditional asset

intermediaries, stock & FX brokers

Equity | Forex | Derivatives | Fixed Income

Explore VenuesIndustry Leaders Trust Our Institutional-grade Crypto Trading Platform

Crypto banking institutions, hedge funds, asset managers, and recognized partners trust Wyden‘s team of trading system veterans and crypto asset experts to deliver best-in-class technology. This is why our institutional crypto trading platform meets the highest institutional needs.

SCRYPT Digital was built to serve institutions, so we are thrilled to be partnering with AlgoTrader to help increase its level of liquidity for its institutional client base. As SCRYPT Digital has 24/7/365 access and 99.99% uptime, we offer optimal trading conditions and superior execution.

Norman WoodingCEO

The addition of AlgoTrader will help LevelField build out the digital asset side of the business, and to facilitate our vision of growing into a full-service financial services firm.

Gene A. Grant IIFounder & CEO

InCore Bank clients now have 24/7 access to deeply liquid global crypto markets through a range of venues, providing faster trading and settlement and supporting a wider range of assets.

Mark DambacherCEO

Metaco and Wyden are united by a strategic partnership since 2019 to offer an integrated technology stack to financial institutions – covering every step from digital asset custody and management to trading, execution and automation.

Adrien TreccaniFounder and CEO

We scaled our trading systems across more exchanges & pairs with AlgoTrader's agnostic and robust platform, resulting in a stronger business focus and less time spent on technical details.

Luke SchwartzkopffCo-Founder

The advanced feature suite meets the need of a modern fund manager – from trade execution management to automated rebalancing and monitoring we trust AlgoTrader’s mission-critical infrastructure.

Miró MitevFounder & CEO

Clearly the best software solution for crypto quantitative trading on the market. AlgoTrader connects you to all major digital asset liquidity venues & instruments and fully supports trade automation.

SvenCEO

AlgoTrader fits extremely well with our data-driven approach as we use the integrated development environment for our innovative crypto investment solutions.

Katharina GehraManaging Director

We use AT QUANT to operate our Forex trading strategies which offers great customizability due to its open-source architecture and integrations. We also highly value the AlgoTrader team's support and expertise.

Hugo CoryFounderSCRYPT Digital was built to serve institutions, so we are thrilled to be partnering with AlgoTrader to help increase its level of liquidity for its institutional client base. As SCRYPT Digital has 24/7/365 access and 99.99% uptime, we offer optimal trading conditions and superior execution.

Norman WoodingCEOThe addition of AlgoTrader will help LevelField build out the digital asset side of the business, and to facilitate our vision of growing into a full-service financial services firm.

Gene A. Grant IIFounder & CEOConnect with us!

Get In Touch